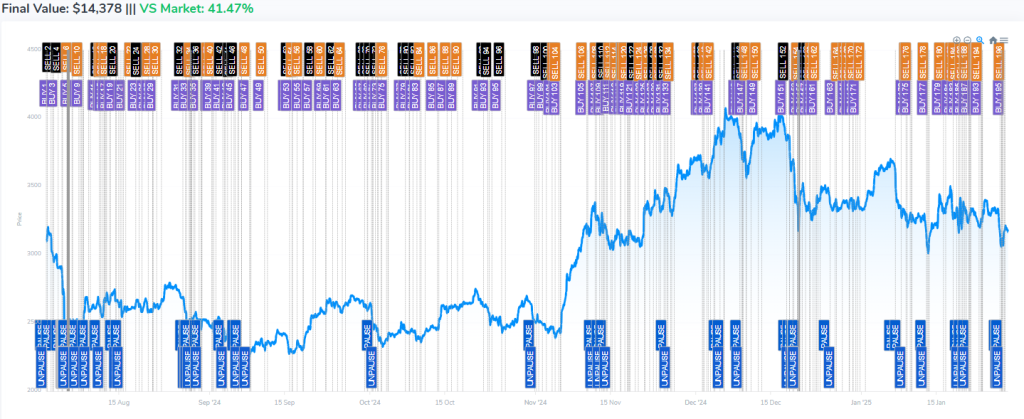

Learn how our algorithmic trading works

Strategy Development: Traders or quantitative analysts (quants) develop algorithms based on specific trading strategies. These strategies can range from simple to highly complex and can be based on various factors such as price movements, technical indicators, statistical arbitrage, market liquidity, and more.

Coding the Algorithm: Once a strategy is conceptualized, it needs to be coded into a computer program. This involves using programming languages such as Python, C++, Java, or specialized algorithmic trading platforms that offer coding interfaces.

Data Collection and Analysis: Algorithms require data to make informed decisions. This data can include historical price data, real-time market feeds, news feeds, economic indicators, and more. Traders need to ensure the data is accurate and timely for effective algorithmic trading.

Backtesting: Before deploying an algorithm in real-time markets, it’s crucial to backtest it using historical data. Backtesting helps evaluate how the algorithm would have performed if it had been used in the past. This step helps in refining the strategy and identifying potential pitfalls.

Deployment: Once an algorithm passes the backtesting phase, it can be deployed in live markets. Algorithms can be set up to trade automatically through direct market access (DMA) platforms provided by brokers or through dedicated trading servers colocated near exchanges for lower latency.

Monitoring and Maintenance: Even after deployment, algorithms require monitoring. Market conditions change, and algorithms may need adjustments to remain effective. This monitoring ensures that the algorithm continues to perform as expected and adheres to risk management protocols.

Execution: When market conditions meet the criteria defined by the algorithm, it automatically executes trades. Algorithms can execute trades at speeds much faster than human traders, taking advantage of fleeting opportunities in the market.

Latency is a critical issue to overcome and requires a data collection and processing techniques that execute in milliseconds.

Risk Management: Effective algorithmic trading strategies include risk management protocols to limit potential losses. This can include setting stop-loss orders, position size limits, and monitoring overall exposure.

Performance Evaluation: Traders continuously evaluate the performance of their algorithms. Metrics such as profitability, Sharpe ratio, drawdowns, and consistency are analyzed to determine the algorithm’s success and whether adjustments are needed.

Regulatory Compliance: Algorithmic trading is subject to regulatory oversight in many jurisdictions. Traders must comply with regulations concerning fair trading practices, market manipulation, and system integrity.

Overall, algorithmic trading aims to remove human emotions from trading decisions, execute trades swiftly, capitalize on market inefficiencies, and optimize trading strategies based on data analysis and historical performance.